Are you wondering what other small business owners in Canada pay for insurance? Whether you operate in Toronto, Vancouver, Calgary or Halifax, it is important to protect your business with the right amount of insurance.

Canadian business owners often wonder if they are overpaying for their premiums. While insurance premiums fluctuate depending on some factors (more on this in later), it is useful to have a general idea of what other Canadian small business owners are paying to protect themselves.

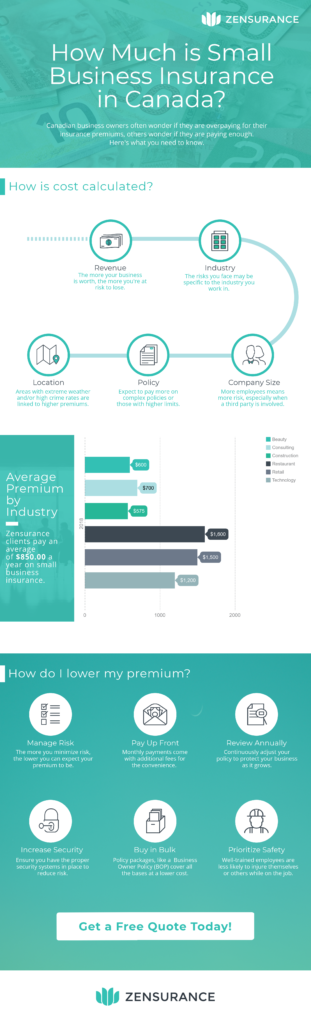

Zensurance customers, a majority of who are small business owners, pay $850 per year on average for insurance, but it is important to remember that the number varies quite a bit depending on what industry they operate in.

How is your business insurance cost calculated?

Do you work with your hands? Do you provide advice to your clients? Do you own substantial office space or inventory? These are some of the questions that go into determining how much any individual business will pay for its insurance premium.

Insurance companies’ underwriters take into account many risk factors, such as business type, industry, business size, yearly revenue, location, etc. They also maintain historical records of these risk factors and use mathematical models to calculate the odds of insurance claims based on different combinations of these factors. As a result, the cost of business insurance for every individual business varies quite a bit.

What factors affect the cost of your insurance premium?

Here is a list of factors that determine policy pricing for various insurance types:

- Do you operate in a high-risk industry?

- What kind of goods or services do you sell?

- What is the total value of the property you own?

- How much revenue did you earn last year?

- How much revenue do you expect to earn next year?

- How many employees do you have?

- How much experience do you have in running operations in your industry?

- Have you had insurance claims in the past?

Related Posts

Sign Up for ZenMail

"*" indicates required fields

Why do prices vary so much?

In an ideal scenario, nobody would ever have to file an insurance claim, but unfortunately, risk is unavoidable, and accidents can happen anywhere, any time. Also, accidents are more likely to happen in some places than others, and some accidents cost a lot more than others.

For example, a fire at a major wholesaler’s warehouse would damage property worth a higher dollar amount than a fire at a consultant’s office.

The more you are able to minimize the risks that your business is exposed to, the more you can expect to lower your insurance premium. On that note, here’s another important question that concerns small business owners: how to lower insurance costs?

How to lower business insurance premiums?

Small business owners purchase insurance to protect themselves from the possibility of having to lose their life savings due to a costly claim. That being said, the peace of mind that comes with insurance comes at a cost.

As a business owner, what can you do to reduce your insurance premium ? Here are some tips:

- Take security precautions – preventing a problem costs less than fixing it. Make sure you have the right security systems, fire sprinklers, burglary and theft prevention measures, worker safety programs in place to minimize the risks that you are exposed to. If you handle sensitive customer data, make sure to take cybersecurity measures [link] to reduce your exposure to cyber risks [link]

- Pay up-front – paying a lump-sum can be somewhat of a burden, but if you are able to afford doing so, it is cheaper than a monthly payment plan. If that is not possible right now, plan to put some money aside to take advantage of lump-sum discounts for the next fiscal year.

- Re-evaluate annually – changes happen constantly. Insurance premiums are renewed on an annual basis, and that is more than enough time for substantial changes to take place in your business. The next time you are about to renew your policy, call your insurance broker to check if changes in your business make you eligible for a different policy. If that sounds like too much work, you can also get a business insurance quote online in a matter of minutes.

Learn more about different business insurance types

Business insurance is an umbrella term that refers to many different types of policies. These are the most common types of policies that small businesses require:

Commercial General Liability (CGL) – this is the most basic policy required by businesses. It protects businesses if they are found legally liable for injuries to a third party caused by their products or services. If insurance was Thanksgiving, CGL would be the turkey. You can’t have Thanksgiving without the turkey

Professional Liability Insurance– also known as Errors and Omissions Insurance, is an essential policy for small businesses that provide a service. A professional liability policy protects the business owner from claims of errors and omissions in their services to their clients.

Commercial Property Insurance – if you own a large office space, inventory or expensive equipment, you have probably spared some thought to the possibility of perils such as fire, flood and theft. A commercial property policy will cover protect your property which is essential for the day-to-day operations of your business.

If you own large office space, costly inventory or expensive equipment, protect your property with a commercial property policy. Fire, flood or theft can cripple a small business so it is important to insure everything that is valuable.

Other types of policies worth looking into:

Can I save money on my current insurance policy?

Most people can, but of course, it’s not realistic to expect small business owners to keep dialing different brokers. Fortunately, insurance is evolving. Small business owners can now get a free online insurance quote in a matter of minutes and compare it to their current policy. No more excuses to throw away money.

Recent Posts

What Landlords Need to Know About Student Rental Housing Insurance

Canadian landlords with properties near universities and colleges have an excellent opportunity to meet the constant demand for off-campus student rental housing. But renting to students carries real risks, and property owners need to safeguard their investments against damage and lawsuits. Here's how the right insurance helps.

10 Essential Types of Business Insurance for Small Businesses in Canada

Unexpected challenges can derail even the most determined small business owner. Here are the 10 types of business insurance every Canadian small business should know about, and how to get covered for less.

Back to School: 9 Reasons Why Tutors and Teachers Need Insurance

As a new school year begins, it’s not just lesson plans that need reviewing – your protection does, too. From liability claims to unexpected accidents, educators in Canada face real risks. Here’s what tutors and educators need to know to stay focused on what they do best: teaching.